Inside wealth management products

The wealth management industry is focused on helping individuals, families, and institutions grow, protect, and transfer wealth over the long term through a combination of investment management, financial planning, tax-aware strategies, and estate and trust services. The industry operates at the intersection of finance, regulation, and human judgment, serving clients whose financial decisions carry lifelong and often multigenerational consequences.

The ecosystem includes large private banks and wealth divisions of global financial institutions such as JPMorgan Chase, Bank of America, and UBS, alongside independent registered investment advisors (RIAs), broker-dealers, trust companies and custodians like Charles Schwab.

A wealth management product is a professional-grade system that enables financial advisors and firms to manage client wealth responsibly, compliantly, and at scale. Unlike consumer finance apps, it is not designed for casual self-service, it is built to support licensed professionals making high-stakes, regulated decisions on behalf of clients.

Building a wealth management product is as much an organizational challenge as it is a technical one, given the regulatory, financial, and fiduciary stakes involved. To manage this complexity and risk, firms rely on deliberately structured teams that combine strategic oversight, domain expertise, and disciplined execution.

Product teams operate in close coordination with advisors, legal, compliance, risk, and privacy functions because every decision directly affects regulated workflows and real client outcomes.

As AI adoption increases, privacy and data governance have become even more central, introducing requirements around explainability, data lineage, and auditability that product teams must address from day one. In practice, leading in this environment is less about selling a big vision and more about keeping stakeholders aligned, as leadership attention tends to center on regulatory safety, advisor productivity, platform reliability, and cost discipline.

Firms that fail to invest in product often struggle to modernize and place heavy operational strain on advisors, while leading organizations treat product as the bridge between regulatory requirements, technology, and day-to-day advisor workflows. Innovation may move slower than in SaaS, but by design; when workflows improve, the impact scales across thousands of advisors and billions in assets, setting the stage for why AI is now top of mind for wealth management leaders.

Why AI is top of mind for wealth management leaders

In most wealth management leadership discussions, AI is top of mind as a necessary response to mounting pressure to scale advice, control risk, and maintain trust in increasingly complex operating environments.

But when teams move from strategy decks to real delivery, that ambition quickly collides with reality. Conversations with engineers, advisors, operations, and compliance tend to circle the same questions: What problem are we actually solving? Where does AI add value instead of complexity? How do we ship something explainable, compliant, and genuinely useful?

After working across multiple advisory platforms and wealth products, a consistent pattern becomes hard to ignore. AI succeeds in wealth management when it removes real workflow pain and supports professional judgment at scale. It fails when it is treated as a capability in search of a problem.

What follows is not a vision of what AI could do, but an account of what has worked in production, what stalled quietly, and what surprised teams once real advisors and operators began using it.

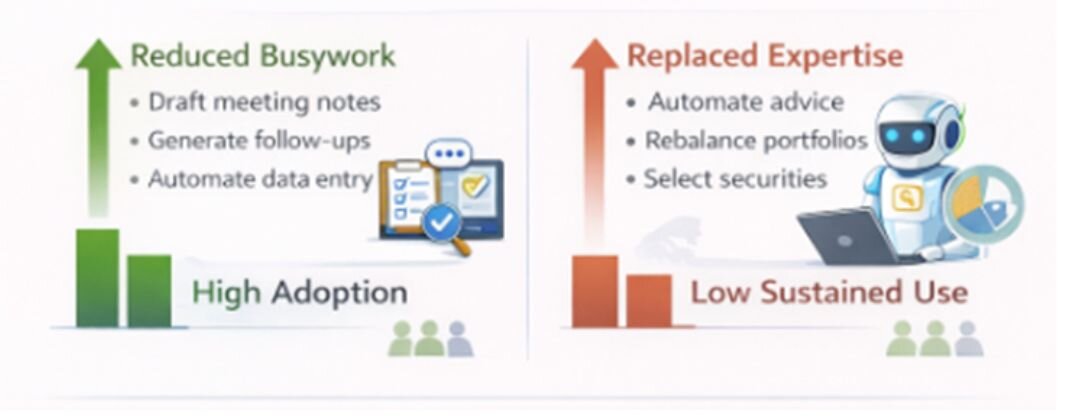

Start with administrative fatigue

Spend a day shadowing a financial advisor and a contradiction becomes obvious.

Most advisors chose the profession to work with people, yet much of their time is spent working with software. Meeting notes need to be written, CRM records updated, follow-up emails drafted, and the same information re-entered across multiple tools. As platforms become more “digital,” the advisor experience often becomes more fragmented rather than simpler.

The AI features that gained early traction did not try to replace portfolio construction or investment judgment. They focused on the invisible work that happens after the meeting. Drafting meeting summaries. Capturing key decisions. Generating follow-ups. Updating internal systems without forcing advisors to repeat themselves.

When these tasks became faster or disappeared entirely, adoption followed naturally. Advisors didn’t feel like AI was changing their role; it simply removed friction from the parts of the job they never enjoyed.

The teams that succeeded didn’t begin by debating model architectures. They began by listening to what frustrated advisors once the client left the room.

Why trust matters more than accuracy

One team introduced AI-generated meeting summaries designed to populate CRM records automatically. On paper, the feature was successful: summaries were accurate, structured, and consistent. In practice, adoption lagged.

The issue wasn’t quality, it was control.

Advisors were uncomfortable with content being saved on their behalf. Small errors felt risky, even if they were rare. The solution turned out to be simple but decisive: summaries were generated after the meeting, surfaced as drafts, and required explicit advisor review before being saved.

Once advisors could edit, approve, or discard suggestions, usage increased rapidly. Over time, the system learned from edits and improved, but the real unlock was trust, not intelligence.

In regulated environments, perceived control often matters more than raw accuracy. AI features that acknowledge this tend to survive long enough to improve.

Personalization is an experience problem

For a long time, personalization in wealth management was reduced to a narrow choice among a few predefined risk profiles, conservative, balanced, or aggressive, applied uniformly across clients.

AI did not change the fundamentals of investing or replace modern portfolio theory. What it made possible was the ability to account for real-world complexity at scale: concentrated equity positions, tax considerations, ESG preferences, liquidity needs, and behavioral realities that rarely align neatly with a risk questionnaire.

The most effective platforms recognized that personalization is not primarily an optimization problem. It is an experience design challenge. Preferences surface through conversations, emails, and passing remarks. Advisors interpret those signals and translate them into advice that clients can understand and trust.

AI adds value when it helps convert this unstructured input into clear, explainable constraints that shape recommendations without obscuring the reasoning behind them. When personalization feels like a black box, advisors hesitate to rely on it. When it enables better, more confident client conversations, it becomes a core part of the advisory experience.

Where AI quietly delivers its biggest wins

Some of the most valuable AI work in wealth platforms isn’t generative at all. It’s data unification.

Wealth systems are infamous for duplicate client records, conflicting account identifiers, broken integrations, and critical data living in spreadsheets and email threads. These issues rarely appear in roadmaps or marketing narratives, yet they determine whether any advanced capability can function reliably.

Teams that invested in intelligent matching, reconciliation, and entity resolution unlocked disproportionate benefits. Advisors gained a coherent unified view of clients. Operations teams reduced time spent resolving discrepancies. Product teams finally had a stable foundation to build on.

Many of these efforts were never branded as “AI initiatives,” yet without them, more visible AI features struggled to deliver value. When the underlying data isn’t coherent, even the best models fail often quietly.

How compliance works best as a design partner

Compliance is often seen as a brake on AI, but strong implementations show the opposite. When compliance is involved early and clear about expectations, it helps shape how AI features behave rather than blocking them.

Teams that focused on understanding risk and transparency, rather than pushing AI “through” compliance, built better products. Alerts explained their triggers, decision context was logged automatically, and supervisors reviewed patterns instead of chasing exceptions.

Compliance didn’t slow delivery. It became part of the design discipline, grounding AI behavior in policy and regulation.

Why some AI features stick while others fade away

AI features gained traction when they removed obvious pain from daily workflows, preserved human judgment, explained outputs in plain language, and fit naturally into existing tools. Success was measured in minutes saved, errors avoided, or clarity gained.

They struggled when they launched as innovation pilots without clear ownership, attempted to replace expertise instead of supporting it, or added steps rather than removing them. In those cases, even technically impressive systems failed to earn trust.

In wealth management, AI rarely fails because it isn’t powerful enough. It fails because it asks users to change behavior without offering enough value in return.

What this means for product teams

Product teams building AI in wealth management don’t need to become machine-learning specialists. The real challenge remains strong product judgment: understanding how advisors and clients actually work, designing for trust and explainability, and embedding technology into existing workflows instead of reshaping workflows around the technology.

AI will continue to advance rapidly. Models will improve and capabilities will expand. But the teams delivering meaningful AI today are not defined by model complexity. They are defined by how closely they stay connected to users and how clearly they articulate the problems they are solving.

In wealth management, AI works when it makes someone’s day easier. Everything else is secondary.